The development of decentralized finance (DeFi) has brought revolutionary changes in the way capital markets operate, especially through the birth of decentralized exchanges (DEX) based on automated market making mechanisms (Automated Market Makers - AMM). In this ecosystem, liquidity provision (Liquidity Providing - LP) has become a popular method of generating passive income, allowing individual investors to act as market makers.

However, according to Tan Phat Digital's analysis, in addition to the profit potential from trading fees and administrative rewards, liquidity providers face a unique and often misunderstood type of risk: Impermanent Loss. temporary ventricle). This is the phenomenon in which the value of a liquidity provider's assets decreases compared to just holding that asset in a wallet when there are strong price fluctuations between token pairs in the liquidity pool. Understanding the mathematical nature, operating mechanism of arbitrageurs, and modern hedging strategies is a prerequisite for optimizing capital efficiency in the volatile DeFi environment.

The nature and operating mechanism of Impermanent Loss in the DeFi ecosystem

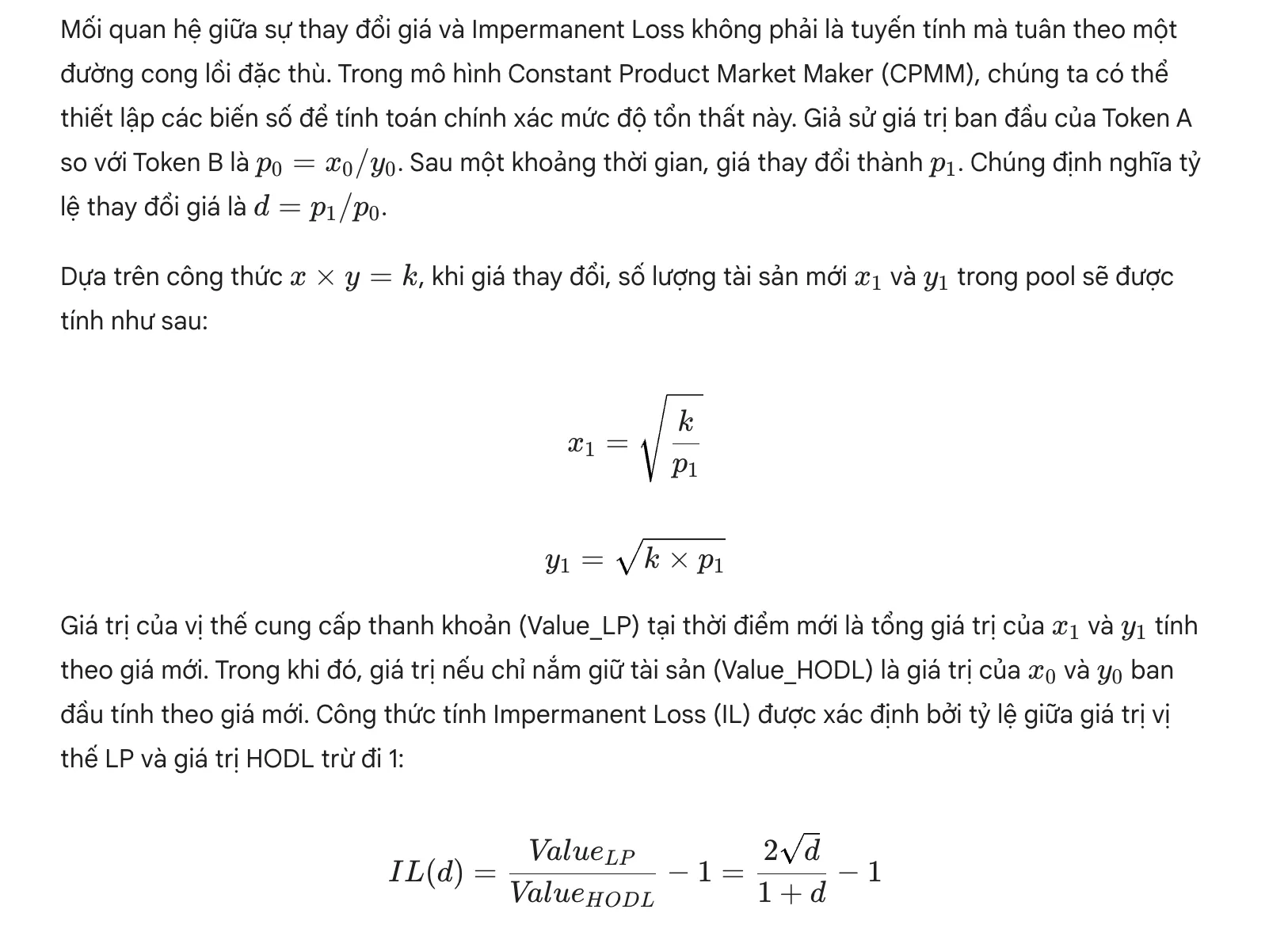

To understand Impermanent Loss, it is necessary to first consider the foundation of most current AMMs such as Uniswap, PancakeSwap and SushiSwap. These platforms operate on a constant product algorithm, often expressed through the equation $x \times y = k$. Where, $x$ and $y$ represent the quantity of two different assets in the liquidity pool, and $k$ is a constant representing the total liquidity. When a liquidity provider deposits assets into the pool, they are usually required to deposit a certain value ratio, most commonly 50/50. This mechanism ensures that no matter how the value of assets changes, their quantity product must remain constant.

Impermanent Loss arises when the prices of these assets on external markets (such as centralized exchanges) begin to decouple from the initial rate in the pool. Since AMM does not automatically update prices based on external data, it relies on arbitrageurs to adjust the ratio of assets in the pool. When the price of Token A skyrockets compared to Token B, arbitrageurs will buy cheap Token A from the pool and sell it outside to make a profit. This process continues until the amount of Token A in the pool decreases and the amount of Token B increases enough for the exchange rate in the pool to equalize with the market price. For the liquidity provider, this means that their portfolio now contains fewer appreciating assets and more depreciating assets than it did initially.

This loss is called "temporary" because it only truly becomes a permanent loss when the user decides to withdraw liquidity from the pool at a time when the rate is skewed. If the prices of the two assets return to the rate at the time of deposit, this loss will theoretically disappear, and the liquidity provider will only collect the accumulated transaction fees. However, in reality, cryptocurrency markets rarely return to absolute equilibrium, making this risk a permanent cost factor for LPs.

Mathematical Analysis and Modeling of Price Volatility

Below is the actual level of loss based on the scenarios Different price fluctuations are compiled by Tan Phat Digital:

Price volatility increased by 25% (d = 1.25x): Temporary loss (IL) is -0.6%.

Price volatility increased by 50% (d = 1.50x): Temporary loss (IL) is -2.0%.

- 300% (d = 4.00x): Interim loss (IL) is -20.0%.

Price volatility increased by 400% (d = 5.00x): Interim loss (IL) is -25.5%.

From the above data, it can be seen that even if the price doubled, the liquidity provider still suffered a loss of 5.7% compared to just holding the token. If the price drops by 50% (d=0.5), the IL loss is equivalent to 5.7% due to the symmetry of the formula. This shows that IL risk always exists regardless of whether the market trend is up or down, as long as there is price divergence between the two assets in the trading pair.

See more: What is Liquidity? How does liquidity affect crypto prices

Concentrated liquidity and risk amplification in Uniswap V3

The birth of Uniswap V3 has brought a major turning point in capital efficiency through the centralized liquidity mechanism (Concentrated Liquidity). Instead of distributing liquidity evenly from price level 0 to infinity, liquidity providers can choose a specific price range ($P_a$ to $P_b$) to deploy their capital. Although this mechanism allows LPs to collect more fees per unit of capital when prices are within range, it also significantly increases the risk of Impermanent Loss.

When liquidity is concentrated in a narrow price range, it creates a virtual leverage effect. Small price changes within this range will result in a much more aggressive rebalancing of assets than in the V2 model. If the price goes outside the selected range, the LP's entire position will be converted to an asset of a lower value at that time, and they will stop receiving trading fees until the price returns to the range. Reports indicate that more than half of the liquidity providers on Uniswap V3 actually experienced negative returns when factoring in IL, suggesting that centralized liquidity management requires much more proactive and sophisticated strategy.

The centralized liquidity model requires LPs to constantly monitor and adjust the scope (rebalancing) to avoid liquidity becoming inactive. As prices approach the edge of the range, the LP's portfolio will quickly become tilted toward the losing asset relative to the remaining asset, exacerbating the impact of divergent losses. This turns liquidity provision from a passive investment activity into a professional market management exercise.

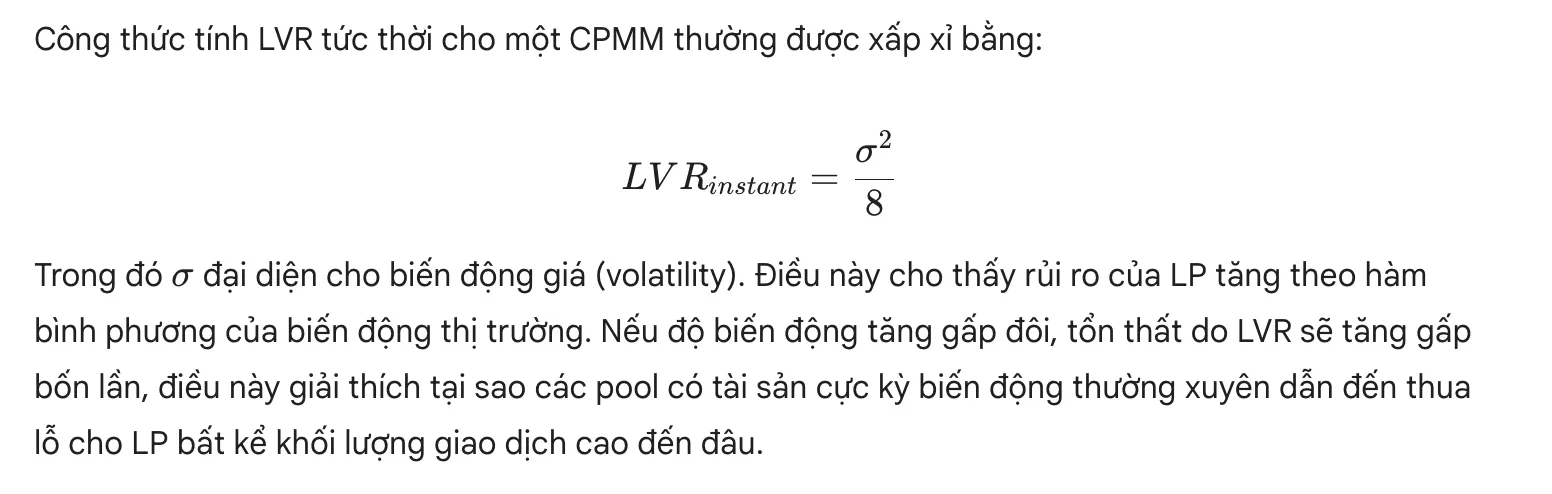

Loss-Versus-Rebalancing (LVR): A new perspective on costs for LPs

In recent years, the DeFi research community has introduced the concept of Loss-Versus-Rebalancing (LVR) as a more accurate measure of the actual costs incurred by liquidity providers. Unlike Impermanent Loss, which compares to a hold (HODL) strategy, LVR compares the performance of LP positions to a strategy of continuous rebalancing on more liquid markets (usually centralized exchanges - CEX).

LVR highlights a harsh truth: liquidity providers are constantly providing cheap "put options" to arbitrageurs. Because AMM always reacts slower than the outside market, arbitrageurs can exploit "stale prices" in the pool to extract profits from LPs. The biggest difference is that while IL can disappear if price returns to its original point, LVR is a path-dependent cost. That is, if the price jumps and then returns, the IL is zero but the LVR is still a large positive number due to the arbitrage transactions that took place during the movement.

Risk mitigation strategy and liquidity portfolio management

Default While Impermanent Loss is an inevitable part of providing liquidity on AMM, Tan Phat Digital recommends that investors can apply a variety of strategies to minimize this impact and optimize net returns.

Choose highly correlated asset pairs and stablecoins

The simplest and most effective way to minimize IL is to provide liquidity to asset pairs with similar price movements or stablecoin pairs. Pairs like USDT/USDC, DAI/USDC or wrapped versions of the same asset (e.g. WBTC/BTC) have a very low risk of price divergence. In these pools, the value of assets moves roughly in parallel, which helps maintain initial deposit rates and allows LPs to safely collect trading fees. However, returns from these pools are often lower due to low risk and high competition from many other capital sources.

Leverage protocols with IL protection mechanisms

Some protocols have integrated insurance or protection mechanisms directly for LPs. A case in point is Bancor V3, which provides instant Impermanent Loss protection to single-sided staking participants. In this model, users only need to deposit a single token and the system will automatically balance liquidity through their BNT governance token. If when withdrawing funds, the asset value decreases due to IL, the protocol will use reserves or accumulated fees to compensate users for the difference. Additionally, protocols like Balancer allow pools to be set up with custom weights (e.g. 80/20 instead of 50/50), helping to minimize exposure to more volatile assets.

Delta-Neutral Strategy and Hedging with Derivatives

For professional investors, using derivatives positions to hedge (hedging) is an important technique. A Delta-Neutral strategy aims to eliminate risks from the movement of the underlying asset price.

Below is a detailed comparison of liquidity management methods based on Tan Phat Digital's experience:

Stablecoin LP Strategy:Provides liquidity for pairs with stable prices (like the USDT/USDC pair).

Levels Risk: Very low.

Complexity: Low.

Correlated LP Strategy: Provides liquidity to same-class or highly correlated assets (like BTC/WBTC).

Risk: Low.

Complexity Complexity: Low.

Bancor ILP Strategy: Leverage loss insurance mechanism built directly into the protocol.

Risk level: Low.

Complexity: Medium.

Strategy Delta-Neutral: Combine borrowing or short positions to balance the Delta index to a neutral level.

Risk level: Low to Medium.

Complexity: High.

Active Management Strategy: Continuously monitor and adjust price ranges (range) in Uniswap V3's centralized liquidity model.

Risk level: Medium to High.

Complexity: Very high.

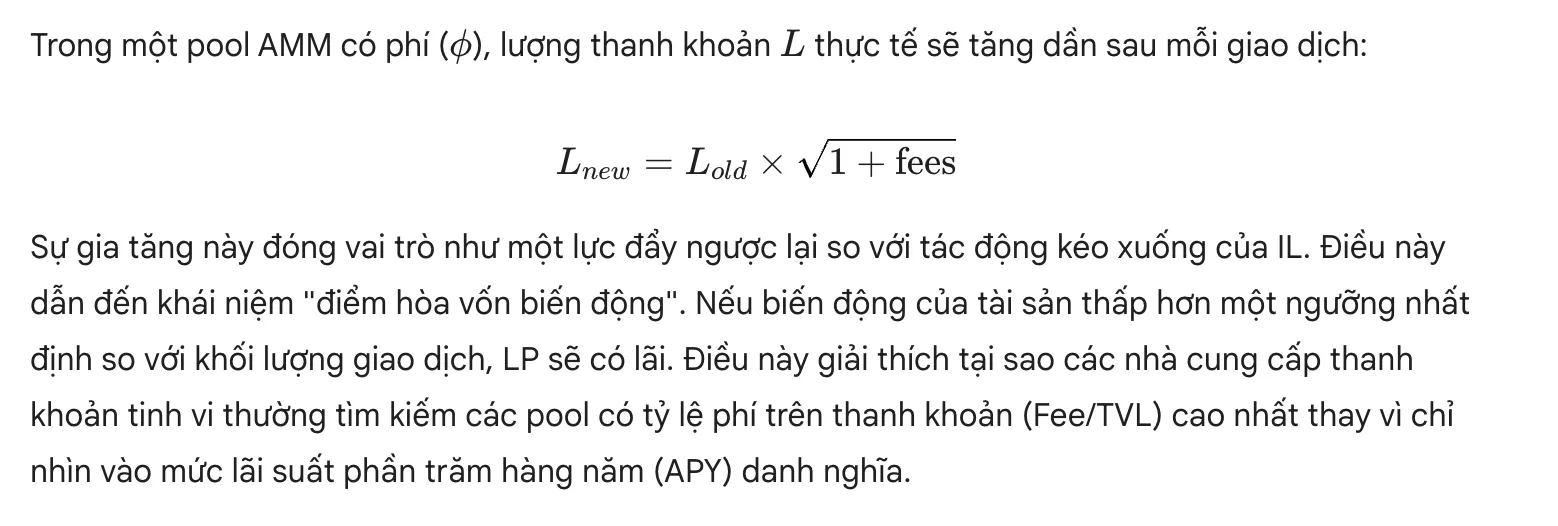

The role of transaction fees and "Impermanent Gain"

An important question for LPs is whether transaction fees are enough to compensate Cover for Impermanent Loss or not. In many cases, the answer is yes, especially in pools with extremely large trading volumes relative to the pool's total liquidity. Recent studies have shown the existence of the "Impermanent Gain" phenomenon, where under conditions of cumulative fees exceeding the rate of price divergence, the liquidity provider actually achieves higher investment efficiency than simply holding.

Automated liquidity management (ALM) tools

The complexity of liquidity management has led to the emergence of Automated Liquidity Management (ALM) services such as Arrakis Finance, Gamma Strategies and Steer Protocol. These platforms act as an intermediary layer, implementing optimization strategies on behalf of LPs.

Gamma Strategies: Use the Hypervisors system to automatically rebalance positions, pool trading fees, and manage price ranges based on quantitative algorithms. Gamma supports over 20 different blockchains, making it highly efficient for retail LPs to access capital.

Arrakis Finance: Focuses on institutional-grade solutions and liquidity management for projects. Arrakis offers strategies like “Flagship” to manage mature pools or “Bootstrap” to support new token issuances, ensuring deep liquidity and minimizing price slippage.

The presence of ALMs eases the time and skill burden on LPs, but also comes with smart contract risks and management fees on the protocol side. Tan Phat Digital notes that entrusting capital always comes with new systemic risks that investors need to consider carefully.

See more: What risks does DeFi pose to newcomers and how to do it? mitigation

The future of liquidity provision and market professionalization

The DeFi market is strongly shifting from the simple liquidity provision stage to the professional market making stage. Impermanent Loss is no longer considered a chance risk but a financial variable that can be calculated and managed. New generation protocols like Uniswap V4 are introducing the “Hooks” mechanism, allowing for extreme customization of liquidity pools. These Hooks can be used to automatically adjust fees based on volatility, help protect LPs better, or automatically execute defensive orders.

In addition, integration between derivatives protocols and AMMs is creating hybrid products, where liquidity provision and hedging are done in the same user interface. This helps reduce the barrier to entry for investors seeking stable returns.

Frequently Asked Questions (FAQs) about Impermanent Loss

1. What really is Impermanent Loss?

Impermanent Loss is the risk that occurs when the prices of the assets you deposit into the liquidity pool change compared to when you deposited them. It is defined as the difference in value between holding assets in a pool and simply holding (HODL) them in a personal wallet.

2. Why is it called a "temporary" loss?

This loss is called "temporary" because it has not been realized (unrealized) on the books as long as you have not withdrawn assets from the pool. If the exchange rate between the two assets returns to the original level at the time of deposit, this loss will disappear.

3. How to accurately calculate Impermanent Loss?

You can use the mathematical formula IL=1+d2d−1, where d is the rate of price change (new price divided by old price). The most realistic way is to compare the total asset value when withdrawn with the value if you kept the original amount of tokens at the current market price.

4. Are transaction fees enough to compensate for this loss?

In many cases, especially in pools with high trading volume and stable price fluctuations, accumulated transaction fees can outweigh temporary losses, creating a net profit for users. However, if the price fluctuates too much (like 2x or 3x), the fee is often not enough to cover it.

5. Is Providing Liquidity for Stablecoins Subject to Impermanent Loss?

IL risk in stablecoin pairs (like USDT/USDC) is extremely low because their price is always anchored at $1. However, IL can still occur if one of the two stablecoins "depeg" causing a large difference in exchange rates.

6. How to minimize the risk of Impermanent Loss?

Tan Phat Digital recommends that you choose asset pairs with high price correlation, use stablecoin pools, or take advantage of platforms with IL insurance mechanisms such as Bancor. In addition, the use of Delta-Neutral defense strategies is also a method of improving efficiency.

7. How does Impermanent Loss affect Yield Farming?

In Yield Farming, users often provide liquidity to new or extremely volatile token pairs to receive high rewards. The IL risk here is very high and can "eat away" all rewards (incentives) if the token price fluctuates uncontrollably.

8. When does a "temporary" loss become a "permanent" loss?

The loss becomes permanent (permanent loss) right at the moment you make an order to withdraw assets from the pool while the exchange rate is still deviating from the time of deposit. At this point, the number of tokens you receive back has been rebalanced and can no longer return to its original state.

9. Do highly volatile currency pairs have higher IL risk?

Definitely yes. The greater the price divergence in asset pairs (e.g. one currency rises sharply, the other falls or stays flat), the more severe the temporary losses. This risk increases exponentially compared to price fluctuations.

10. Should we continue to provide liquidity if we are experiencing IL losses?

This decision depends on your expectations of the price. If you believe that the price will return to the original rate or that future transaction fees will cover the loss, you can continue to hold. If the price divergence trend continues, cutting losses early may be a safer option.

Impermanent Loss is a silent risk but has a huge impact on the effectiveness of investment strategies in DeFi. It is a direct result of the contradiction between the AMM's automatic rebalancing mechanism and the free fluctuations of the external market. Understanding the mathematics behind price divergence helps investors see through the hidden costs of providing liquidity.

Tan Phat Digital believes that, while this risk is always present, the DeFi ecosystem has been developing powerful tools to manage it. The professionalization of liquidity provision, combined with Delta-Neutral strategies and derivatives, is ushering in a new era. In the future, as AMM protocols continue to improve with dynamic fees and flexible Hooks mechanisms, Impermanent Loss will be better controlled, contributing to a more sustainable and efficient decentralized financial market for everyone.

Share